Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Stocks May Be Volatile, but Home Values Aren’t

Stocks May Be Volatile, but Home Values Aren’t

With all the uncertainty in the economy, the stock market has been bouncing around more than usual. And if you’ve been watching your 401(k) or investments lately, chances are you’ve felt that pit in your stomach. One day it’s up. The next day, it’s not. And that may make you feel a little worried about your finances.

But here’s the thing you need to remember if you’re a homeowner. According to Investopedia:

“Traditionally, stocks have been far more volatile than real estate. That’s not to say that real estate prices aren’t ever volatile—the years around the 2007 to 2008 financial crisis are just one memorable example—but stocks are more prone to large value swings.”

While your stocks or 401(k) might see a lot of highs and lows, home values are much less volatile.

A Drop in the Stock Market Doesn’t Mean a Crash in Home Prices

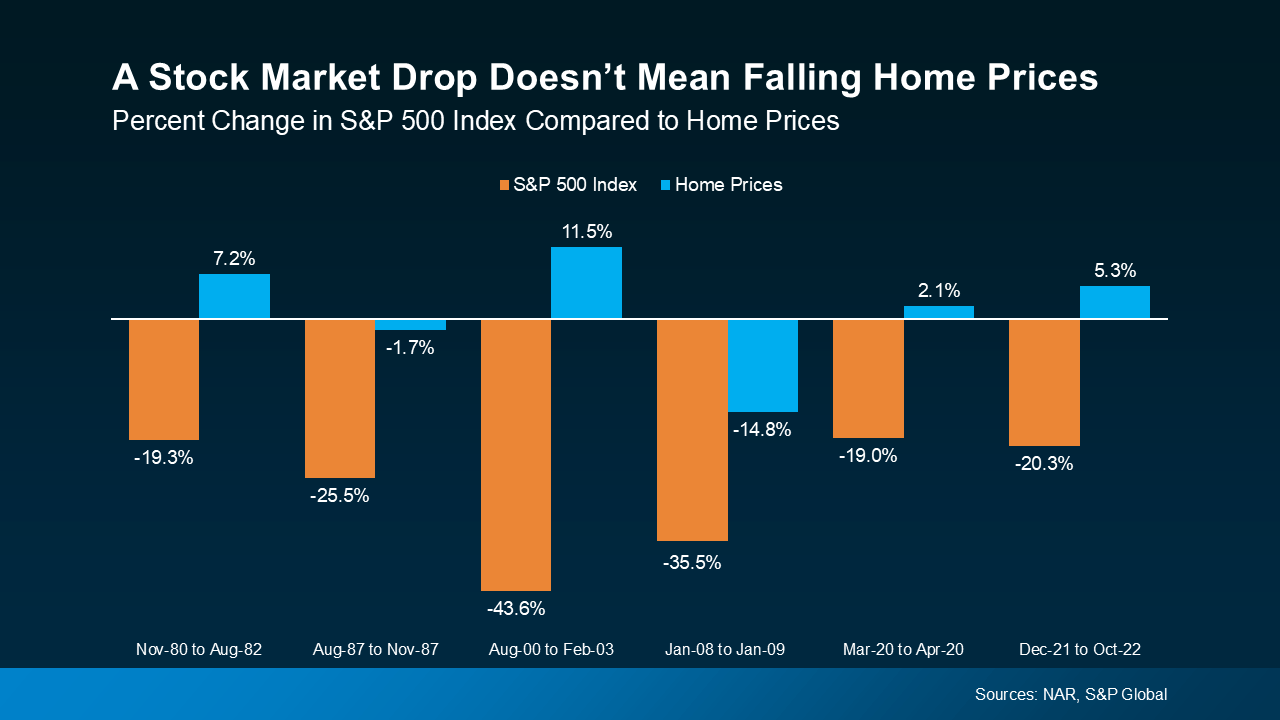

Take a look at the graph below. It shows what happened to home prices (the blue bars) during past stock market swings (the orange bars):

Even when the stock market falls more substantially, home prices don’t always come down with it.

Even when the stock market falls more substantially, home prices don’t always come down with it.

Big home price drops like 2008 are the exception, not the rule. But everyone remembers that one. That stock market crash was caused by loose lending practices, subprime mortgages, and an oversupply of homes – a scenario that doesn’t exist today. That’s what made it so different.

In many cases before and after that time, home values actually went up while the stock market went down, showing that real estate is generally much more stable.

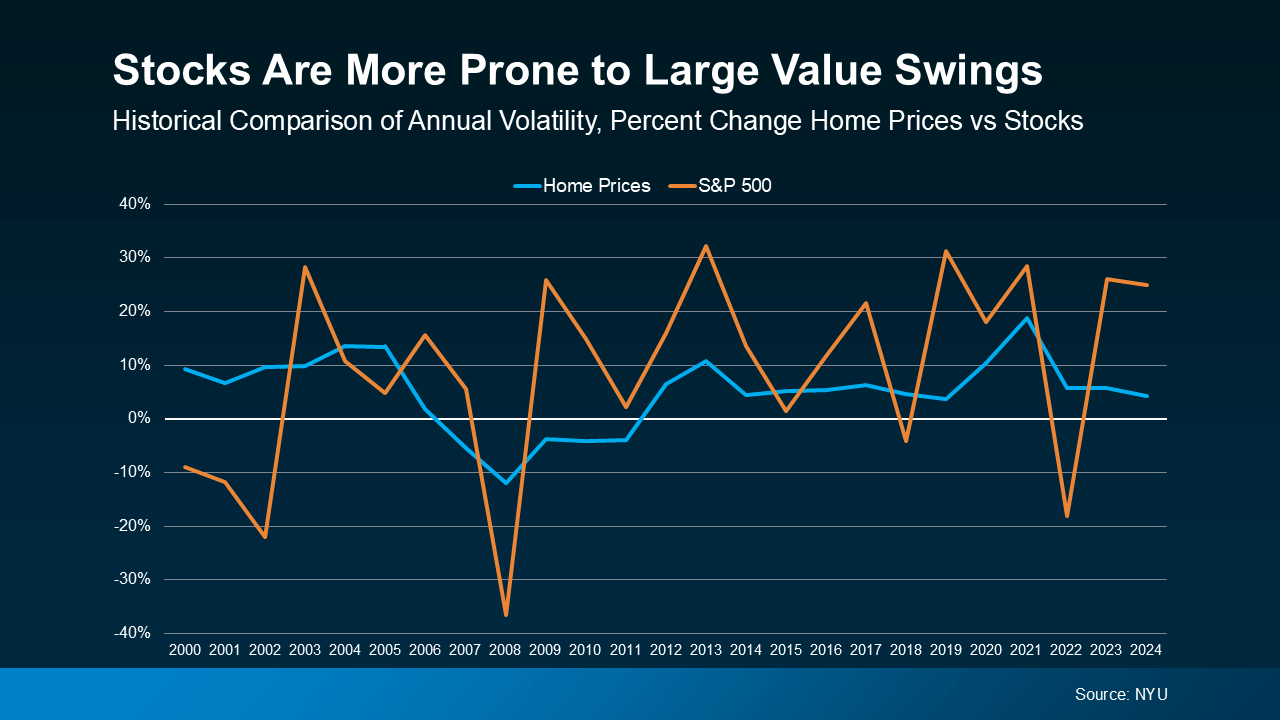

This graph shows how stock prices go up and down (the orange line), sometimes by more than 30% in a year. In contrast, home prices (the blue line) change more slowly (see graph below):

Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.

Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.

That’s why real estate can feel more stable and less risky than the stock market.

So, if you’re worried after the recent ups and downs in your stock portfolio, rest assured, your home isn’t likely to experience the same volatility.

And that’s why homeownership is generally viewed as a preferred long-term investment. Even if things feel uncertain right now, homeowners win in the long run.

Bottom Line

A lot of people are feeling nervous about their finances right now. But there’s one reason for you to feel more secure – your investment in something that’s stood the test of time: real estate.

The 20% Down Payment Myth, Debunked

The 20% Down Payment Myth, Debunked

Saving up to buy a home can feel a little intimidating, especially right now. And for many first-time buyers, the idea that you have to put 20% down can feel like a major roadblock.

But that’s actually a common misconception. Here’s the truth.

Do You Really Have To Put 20% Down When You Buy a Home?

Unless your specific loan type or lender requires it, odds are you won’t have to put 20% down. There are loan options out there designed to help first-time buyers like you get in the door with a much smaller down payment.

For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants, like Veterans. So, while putting down more money does have its benefits, it’s not essential. As The Mortgage Reports says:

“. . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . . the 20 percent down rule is really a myth.”

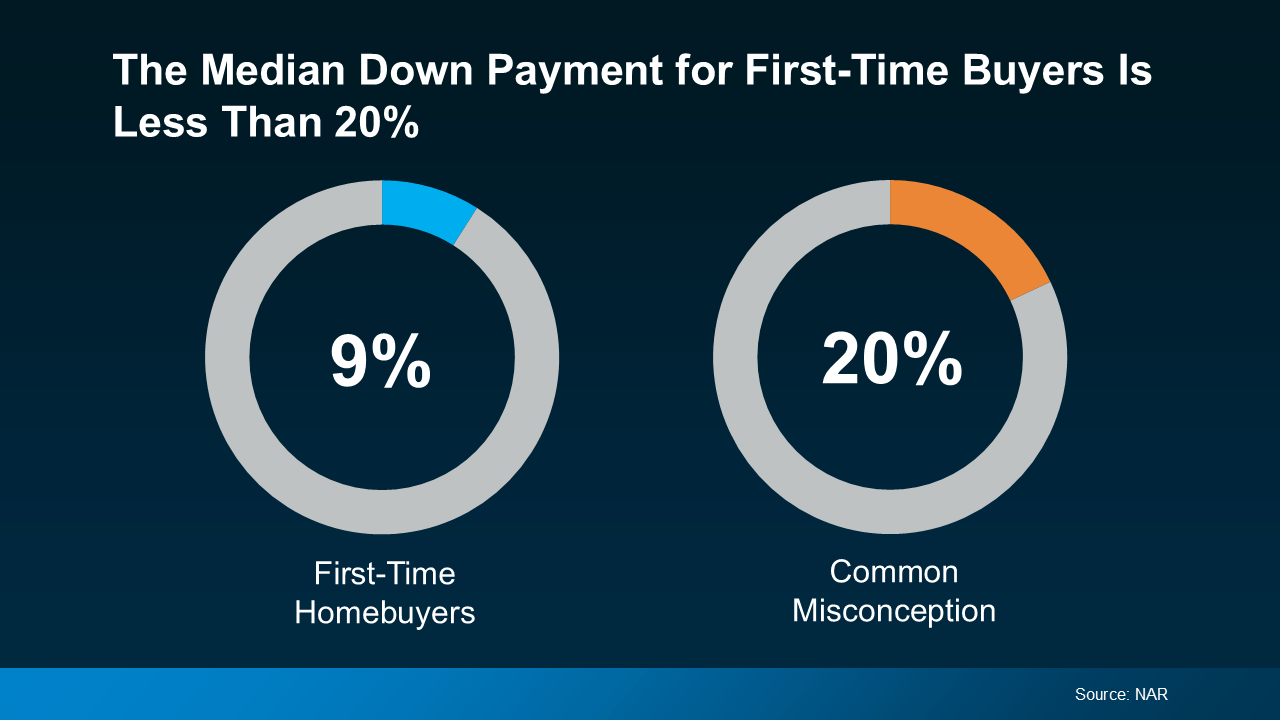

According to the National Association of Realtors (NAR), the median down payment is a lot lower for first-time homebuyers at just 9% (see chart below):

The takeaway? You may not need to save as much as you originally thought.

The takeaway? You may not need to save as much as you originally thought.

And the best part is, there are also a lot of programs out there designed to give your down payment savings a boost. And chances are, you’re not even aware they’re an option.

Why You Should Look into Down Payment Assistance Programs

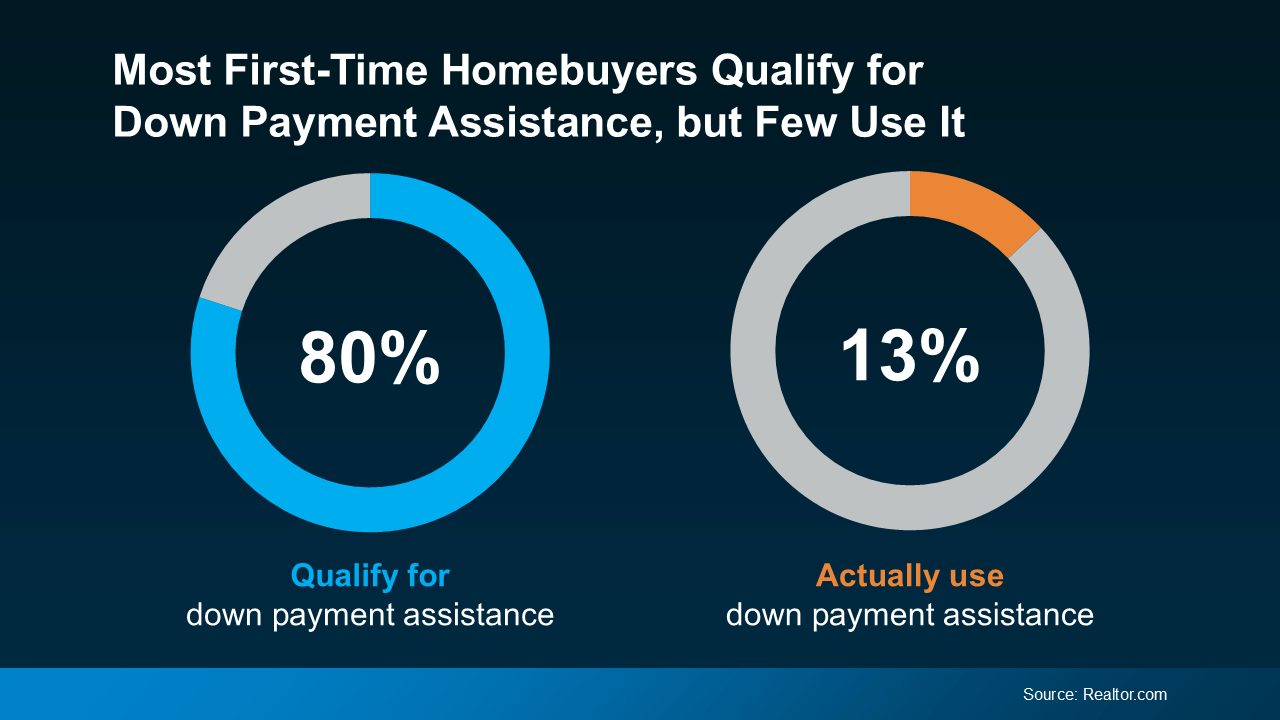

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

That’s a lot of missed opportunity. These programs aren’t small-scale help, either. Some offer thousands of dollars that can go directly toward your down payment. As Rob Chrane, Founder and CEO of Down Payment Resource, shares:

That’s a lot of missed opportunity. These programs aren’t small-scale help, either. Some offer thousands of dollars that can go directly toward your down payment. As Rob Chrane, Founder and CEO of Down Payment Resource, shares:

“Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.”

Imagine how much further your homebuying savings would go if you were able to qualify for $17,000 worth of help. In some cases, you may even be able to stack multiple programs at once, giving what you’ve saved an even bigger lift. These are the type of benefits you don’t want to leave on the table.

Bottom Line

Saving up for your first home can feel like a lot, especially if you’re still thinking you have to put 20% down. The truth is that’s a common myth. Many loan options require much less, and there are even programs out there designed to boost your savings too.

To learn more about what’s available and if you’d qualify for any down payment assistance programs, talk to a trusted lender.